Deferred Tax For Mat Calculation

How To Calculate Profit Or Loss From Balance Sheet Http Www Svtuition Org 2014 11 How To Calculate Profi Accounting Education Learn Accounting Balance Sheet

Trusts Infographic Wealth Management Financial Advice

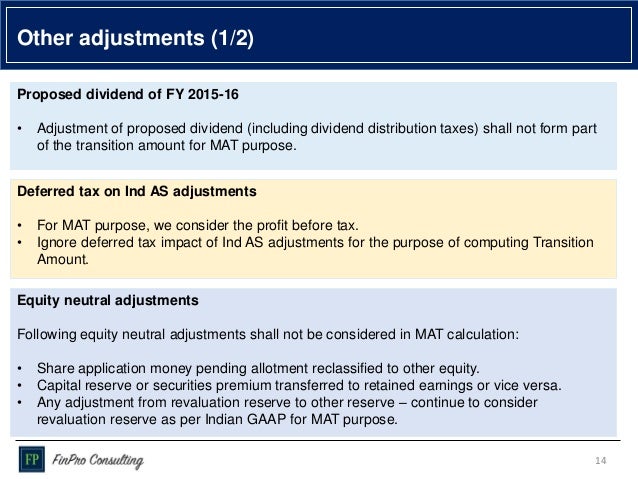

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Tax Reconciliation Under Ias 12 Example Ifrsbox Making Ifrs Easy

Deferred Tax Detailed Analysis With 5 Examples Of Accounting Entries

Proposed Computation Of Mat For Ind As Compliant Companies Taxing Tax

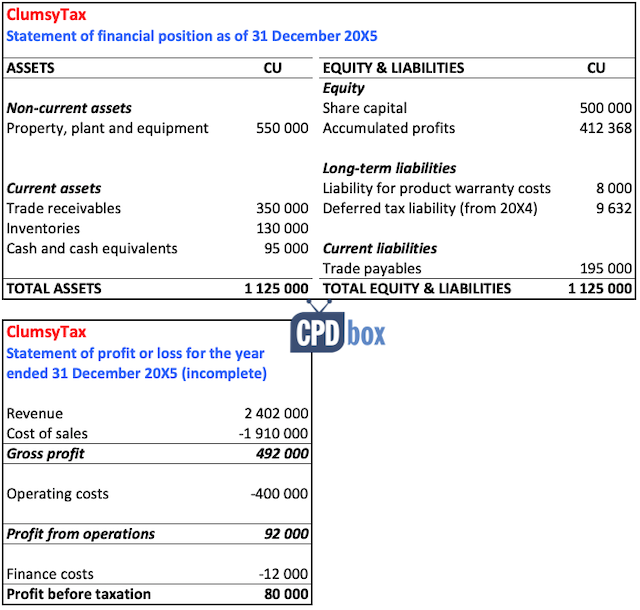

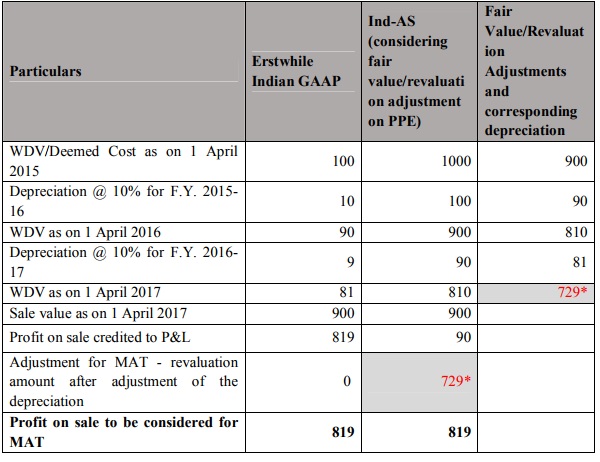

The treatment of deferred tax charge in determining the tax liability under the special provisions of section 115jb of the income tax act is one such case.

Deferred tax for mat calculation. In this article we will be discussing how to calculate deferred tax asset and liability that arises due to depreciation. Deferred tax liability is a tax that is assessed or is due for the current period but has not yet been paid. If depreciation charged for the year as per companies act is rs. 291 000 will be charged back in profit and loss account under tax expenses and rs.

A deferred tax asset is an item on the balance sheet that results from overpayment or advance payment of taxes. Section 115jb levies minimum alternate tax mat at 10 of book profits plus surcharge and cess thereon if such tax is higher than the tax payable under the normal provisions of the act. How to measure deferred tax when a company pays tax as per mat terms to be known. Here an effort is made to comprise all tax computation viz provision for tax mat deferred tax and allowance and disallowance of depreciation under companies act and income tax act in one single excel file.

There are controversies if deferred tax liability debited to p l should be added to the book income for the purpose of mat calculation. Mat a brief introduction. Disclaimer the above calculator is only to enable public to have a quick and an easy access to basic tax calculation and does not purport to give correct tax calculation in all circumstances. It is the opposite of a deferred tax liability which represents income taxes owed.

450000 then accounting profit will differ from it profit. Friends most of us face the challenge of calculating tax as per income tax and as 22. It is the tax effect of timing differences. Minimum alternative tax is payable under the income tax act.

3 09 000 will be shown as deferred tax asset under non current assets. The balance of rs. The continue reading how to measure deferred tax when a company pays tax as per mat. The concept of mat was introduced to target those companies that make huge profits and pay the dividend to their shareholders but pay no minimal tax under the normal provisions of the income tax act by taking advantage of the various deductions and exemptions allowed under the act.

By computing differences in wdv as per it and companies act. Kolkata tribunal in balrampur chini s case has held that the deferred tax liability should not be added back whereas the chennai tribunal in prime textiles ltd case has held otherwise. It is the amount of income tax determined to be payable recoverable in respect of the taxable income tax loss for a period. So deferred tax asset is created which is adjusted with the deferred tax liability of last year.

Ca Final Question Bank Dt Minimum Alternate Tax Mat

Trusts Infographic Wealth Management Financial Advice

Ind As And Mat Provisions Sec 115 Jb Of Income Tax Act

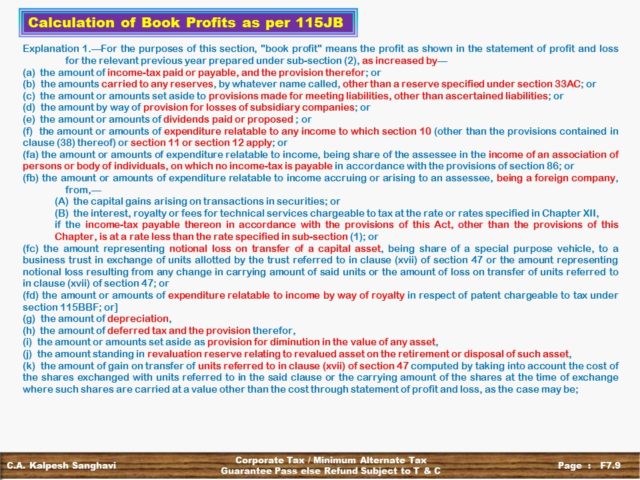

Calculation Of Book Profits For Mat Minimum Alternate Tax Section 115jb

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Cbdt Circular Of Clarifications Faqs On Computation Of S 115jb Book Profit For Ind As Useful Miscellania

Deferred Tax Liability Accounting Double Entry Bookkeeping

Book Profit Definition Examples How To Calculate Book Profit

Calculation Of Book Profits For The Purpose Of Mat Section 115jb

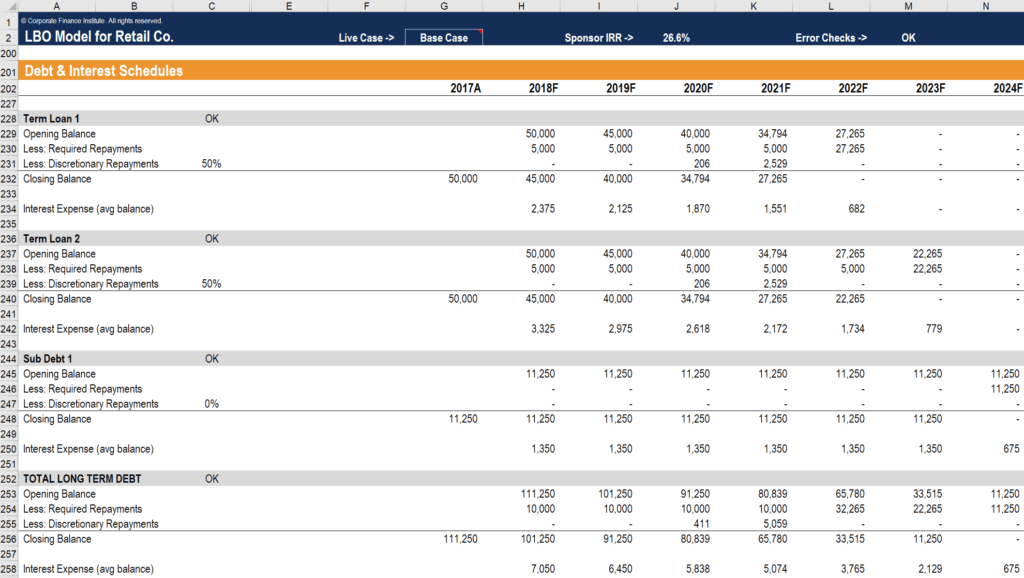

Debt Schedule Timing Of Repayment Interest And Debt Balances

Tax Guide For Rental Investments Side 1 Tax Guide Investing Rental

Deferred Tax Asset Or Liability Its Treatment In Books Of Accounts

Minimum Alternate Tax Or Mat With Detailed Understanding